Why Gold at $2,900 Is CHEAPER Than It Was at $300

Every time Gold surges, the same question pops up:"Did I wait too long? Is Gold too expensive now?"

Nobody wants to buy at the peak, only to watch prices drop.

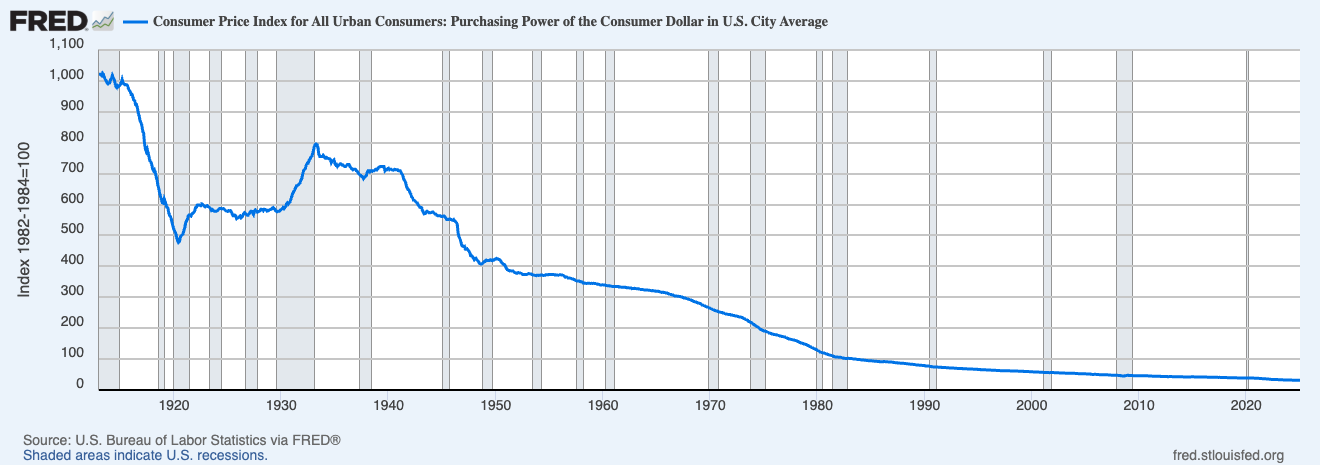

But here’s the hard truth: Gold isn’t getting expensive—your currency is just losing value.

Let’s talk about why the idea that it’s “too late” to buy Gold might be one of the biggest myths in investing—and why, years from now, you might wish you had stacked more at today’s prices.

The Illusion of Price vs. Value

Most people judge Gold by its nominal price—the number they see on the charts. Right now, that number looks high.

But is it really?

To answer that, we need to separate price from value.

Gold is primarily quoted in dollars (or other fiat currencies), and those dollars themselves change in value over time.

Historically, the dollar has lost a staggering amount of purchasing power since the early 20th century—and that means Gold isn’t truly rising—it’s just reflecting the loss of value in paper money.

Let’s look at some key moments in history:

1971 – Gold was $35 per ounce when Nixon ended the Gold standard.

1980 – Gold hit $850, a 2,300% increase in just 9 years. Inflation was running wild, and the dollar had already lost a huge chunk of its value.

2000 – Gold was $250. The dot-com bubble was booming, and nobody wanted Gold.

2011 – Gold hit $1,900, fueled by money printing after the 2008 financial crisis. People said it was too expensive.

2020 – Gold broke $2,000 during the COVID crash and massive stimulus spending. Again, people thought it was too late.

2025 – Gold is now above $2,900, and people still think it’s too expensive.

If you only look at that rise—$35 to $2,000+—it looks like Gold has become astronomically expensive.

But let’s think for a moment:

In 1971, $35 could buy 400 gallons of gas ($0.09/gal). Today, it buys maybe 10 gallons.

In 1971, one ounce of Gold bought ~500 loaves of bread ($0.07/loaf). Today, one ounce of Gold still buys 500 loaves of bread ($5.50/loaf).

So let’s rip off the Band-Aid:

✔ Gold didn’t surge 8,000%. The dollar imploded.

✔ Gold holds its value. The dollar does not.

So when people say Gold is "expensive," what they really mean is: my money doesn’t buy as much Gold as it used to.

Gold Isn’t Just a Commodity - It’s The Ultimate Store of Value

So why does it matter that Gold tracks the true value of money over time? Isn’t it just another commodity whose price goes up and down?

Here’s the thruth:

Gold is not just a commodity; it’s a monetary metal—and central banks know it. That’s precisely why they hoard so much of it.

Unlike currencies that come and go, Gold has held its value for centuries. It doesn’t collapse to zero, it isn’t tied to any single government, and it works across borders and ideologies. Few assets on Earth can claim that kind of staying power.

Just look at how Gold’s purchasing power has held up against major expenses over time.

Case study: buying a home (without crying)

1971 median home price: $25,200 = 720 ounces of Gold ($35/oz)

2025 median home price: $450,000 = 154 ounces of Gold ($2,910/oz)

Translation: Gold became 4.7x more powerful at buying homes since Nixon ended the Gold standard.

Even adjusted for inflation:

1971 home in 2025 dollars: ~$205,000.

154 ounces of Gold today = ~$448,000.

Gold doubled housing’s inflation rate—while cash got crushed.

This pattern holds everywhere:

1971 Ford Mustang: $3,500 = 100 ounces of Gold.

2025 Ford F-150: $60,000 = 20.6 ounces.

Harvard tuition 1971: $2,600 = 74 ounces.

Harvard tuition 2025: $65,000 = 22.3 ounces.

Yes, Gold’s dollar price fluctuates in the short term—sometimes violently—but in the longer run, it maintains its store of value more consistently than any paper currency has over centuries.

Gold Will Keep Rising - Here’s Why

If you’ve been watching Gold’s price action, the surges make perfect sense.

Central banks worldwide are stacking Gold at a historic pace—some estimates suggest over 30% of global Gold production is heading straight into central bank vaults. If the world’s most powerful financial institutions are hoarding Gold, what do they know that the average investor doesn’t?

We live in an era of persistent inflation—not just the typical 2% “target” we’ve heard about for years, but real, biting inflation. In that environment, Gold becomes a safe haven, attracting not just the “Gold bugs” but also institutional investors aiming to hedge portfolios.

De-dollarization is no longer a fringe theory. Multiple nations have openly stated their intention to reduce reliance on the U.S. dollar in global trade. As trust in fiat currencies wavers, Gold becomes an appealing alternative—a neutral, reserve asset outside any single country’s control.

It’s not just central banks piling into Gold—retail investors and mid-sized institutions are following suit. ETFs, mining stocks, Gold-based mutual funds, and physical bullion sales are all surging. And when big money flows into a finite asset like Gold, the price has only one direction to go: up.

With concerns over bank failures, currency crises, energy shocks, and geopolitical turmoil mounting, Gold is in a prime position to keep climbing. Economic uncertainty fuels demand—and right now, uncertainty is everywhere.

Is It Too Late to Buy Gold?

If Gold is already expensive, should you wait for a dip?

History says: probably not.

Sure, we might see temporary pullbacks—$100, maybe even $200 here and there. But new highs don’t automatically mean a crash is coming. In fact, when Gold breaks through major resistance levels with strong momentum, it usually keeps running higher.

These moves aren’t just hype. They’re backed by real economic shifts—inflation, central bank buying, de-dollarization, and growing investor demand.

How frequent are market corrections following all-time highs (based on S&P 500 performance):

Historical bull cycles don’t lie:

1970-1980: +2,300%

2001-2011: +650%

2015-2025: +150%

Every so-called “all-time high” eventually looked cheap in hindsight.

Take the late 1990s, when UK Chancellor Gordon Brown sold a large chunk of Britain’s Gold reserves at $250–$300 an ounce—a decision now seen as a massive mistake. Anyone who bought at those levels has seen 9% average annual growth for decades.

That’s the thing about Gold’s "expensiveness"—it usually only looks expensive until you zoom out.

So How to Afford Buying Gold in 2025? Practical Tips

Now that we’ve established Gold likely isn’t too expensive in a grand historical sense, how do you actually buy?

Dollar-cost averaging (DCA)

A proven technique is dollar-cost averaging—buying in fixed intervals over time, regardless of the short-term price.

How it works:

Buy at fixed intervals (weekly, monthly, quarterly) instead of all at once.

If Gold dips, you buy at a discount.

If Gold spikes, you’ve already built a position at lower prices.

This method smooths out your overall cost basis and removes the emotional "Should I buy now or wait?" dilemma.

If you’re paid monthly, consider setting aside a portion of your paycheck and automating your Gold purchases.

Fractional Gold coins

A common objection is that Gold’s “entrance fee” now feels overwhelming. Dropping two thousand or more dollars on a one-ounce coin can be daunting—especially if you’re new to the precious metals game.

Solution? Fractional Gold coins.

Tenth-ounce coins (~$300)

Quarter-ounce coins (~$700)

Half-ounce coins (~$1,500)

Yes, smaller denominations have higher premiums over spot price, but they also:

✔ Make Gold more accessible

✔ Are easier to sell in small amounts

✔ Can command higher resale premiums if Gold prices surge

Holding physical Gold vs. “paper Gold”

Physical Gold (bullion, coins, bars) offer you tangible ownership and no counterparty risk. Nobody can suddenly freeze your Gold in a third-party account, and you can literally hold your wealth in your hand.

Paper Gold (ETFs, Gold mining stocks, digital allocations) is good for trading and easier to buy or sell in large volumes. However, you do assume additional counterparty risks, and sometimes an ETF or digital contract may not be fully backed by physical metal or might not allow physical redemption.

Most investors do a blend: keep a core portion in physical bullion that you can access if times get truly turbulent, and augment with paper Gold if you want more flexibility or ease of trading.

Asset allocation

Gold isn’t meant to replace your entire portfolio—but it should complement it.

Conservative investors: 5–10% in Gold

Moderate investors: 10–15% in Gold

Inflation hedge or crisis protection: 20%+ in Gold

The right allocation depends on your risk tolerance and macro outlook—but history shows that when fiat currencies weaken, Gold strengthens.

Gold Isn’t Expensive—Your Money Is Just Losing Value

If Gold prices seem high, start small. Fractional coins and gram bars let you build a position without a huge upfront investment.

Worried about premiums? When Gold surges past today’s levels, even higher premiums will seem minor.

Uncertain about timing? Dollar-cost averaging takes the guesswork out of it.

Over and over again, history shows that new highs eventually become old memories, and yesterday’s “expensive” becomes tomorrow’s “steal.”

So, is it too late to buy? Absolutely not.

In a world where fiat currencies continue to lose purchasing power, Gold remains one of the few assets that truly preserves wealth.

Shift your mindset from “Gold is expensive” to “What’s happening to my money?”—and you’ll see why even a small position in Gold could be one of the smartest financial decisions you ever make.

Safe trading,

and remember: All that glitters is not Gold,

Joe