You Don’t Actually Own Your Assets

Why your stocks, your house, and your savings are just complicated promises, and Gold is the only thing you can truly possess.

I had a strange moment the other night. It was around 2 a.m., couldn’t sleep. So I did what any financially-minded person does and opened my brokerage app.

I’m staring at the numbers, the tickers, the things that are supposed to represent my “wealth.” And a really uncomfortable thought bubbled up.

I don’t actually own any of this.

It sounds heretical, doesn’t it?

After all, you have a deed to your house. You have a statement from Vanguard. It all has YOUR name on it.

But what you possess is not the asset itself; it’s a sophisticated, socially-accepted promise. An IOU, held within a complex system you absolutely do not control.

And promises, especially the complicated financial ones, get broken all the time.

It’s time to get brutally honest about the things our financial system tells us are “safe.”

Deconstructing “Safe” Assets

The modern portfolio is built on a foundation of three core asset classes.

But when you apply pressure, you find they aren’t as solid as they appear. They are, in essence, different flavors of counterparty risk.

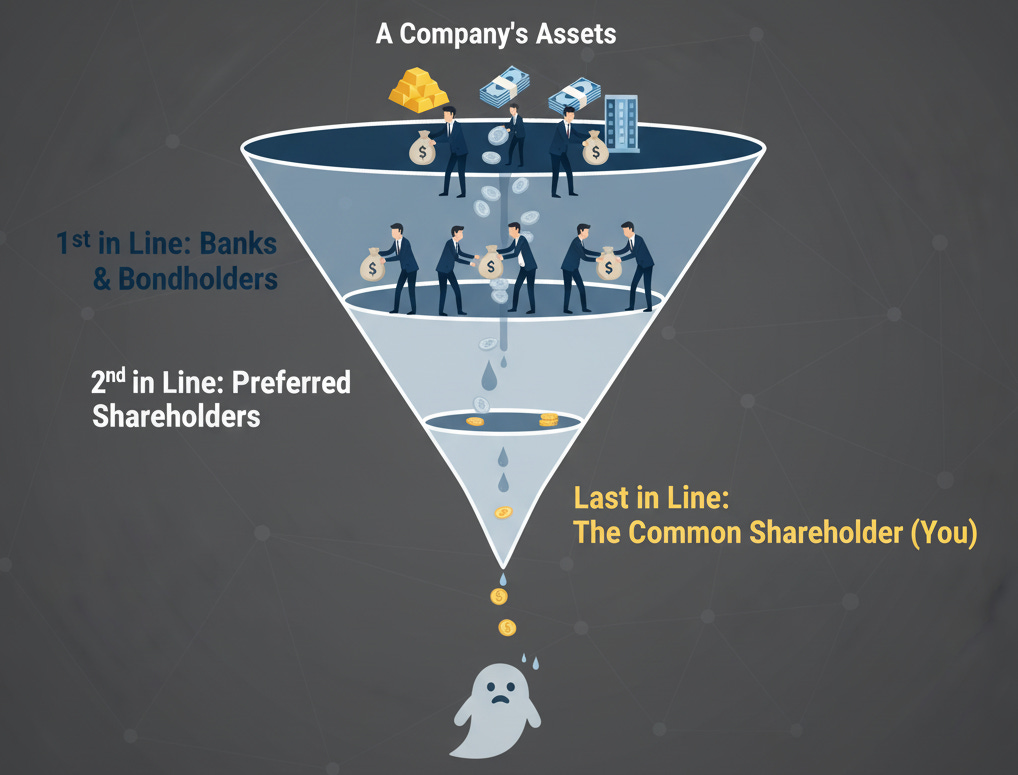

Stocks are just phantom ownership

When you buy a share of a company, you own a piece of paper that says you have a claim on their future earnings. But you’re the last person in line to get paid.

In a bankruptcy, the bondholders, the banks, and the preferred shareholders all get their slice of the pie before you see a single dime.

Often, there’s nothing left.

Remember Lehman Brothers? At $691 billion in assets, it was the largest bankruptcy in U.S. history.

One day it was a titan; the next, shareholders were left with worthless stock certificates. The Dow Jones Industrial Average plummeted 4.5% on the day of the announcement, signaling a massive loss of confidence that spiraled into a global financial crisis.

Enron, Worldcom, General Motors... the graveyard of “safe” companies is enormous.

Your ownership is merely a suggestion, valid only as long as the company thrives and the system governing it remains stable.

Real Estate is just a rental agreement with the state

You think you own your home?

Try this thought experiment: stop paying your property taxes for a few years and see what happens. Eventually, men with guns will show up at your door and inform you who the real owner is.

Beyond that, your ownership is subject to the whims of politics and economics.

The U.S. government has over 200 different statutes that allow them to seize private property (check eminent domain cases).

History is filled with governments confiscating or nationalizing property, like in post-revolutionary Cuba and China. Even in stable economies, a liquidity crisis like 2008 can make your “asset” impossible to sell when you need the cash most.

In hyperinflationary collapses like Weimar Germany or modern-day Venezuela, property becomes a trap - illiquid and immovable thing that traps your capital in a depreciating location and a worthless currency.

Bonds are literally IOUs

This one’s the most honest of the bunch.

A bond is a loan. Its entire existence is based on the promise of repayment.

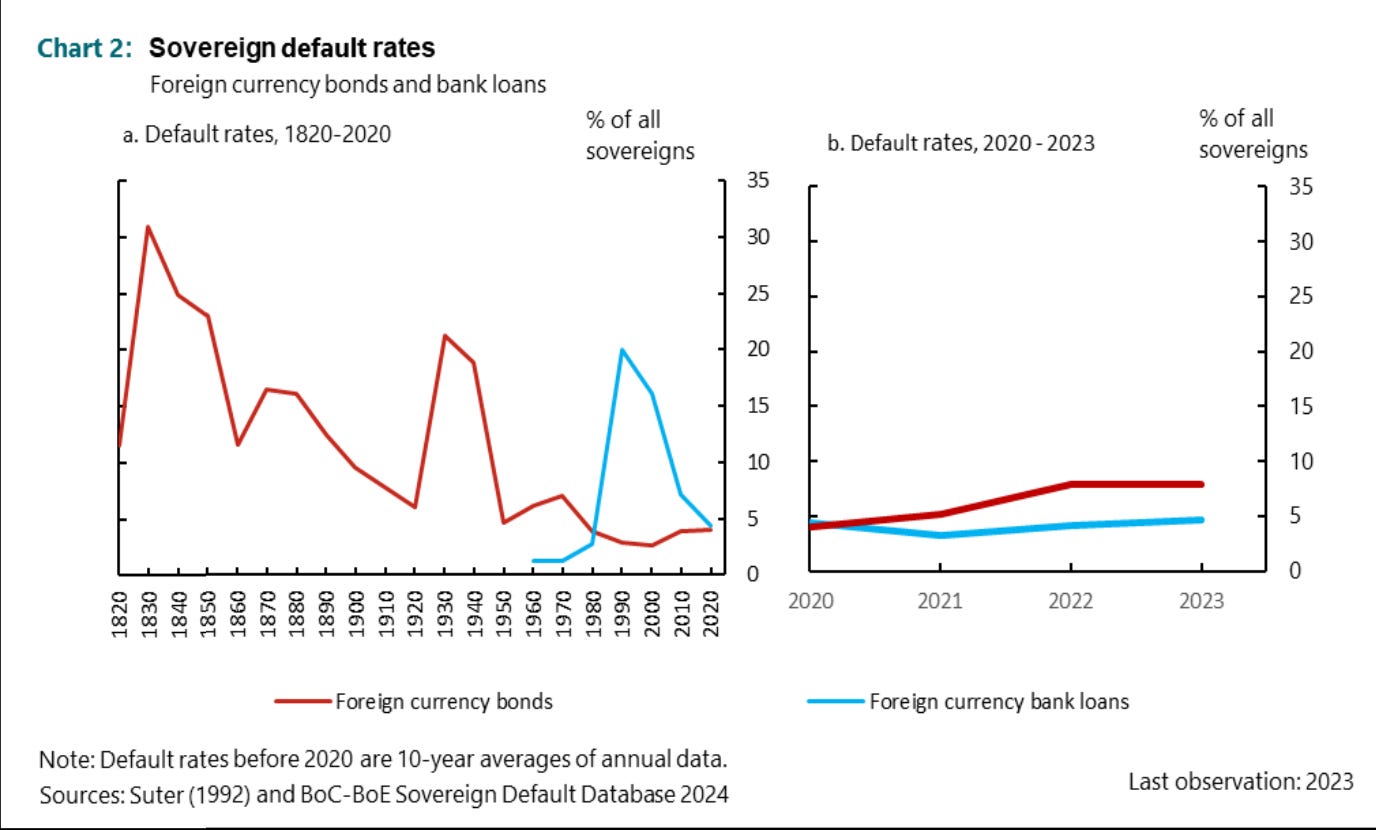

But governments default (all the time).

Spain has defaulted 13 times. Greece has defaulted multiple times since ancient history. Argentina, Russia... the list of sovereign defaults is long and distinguished.

When a government gets into enough trouble, it will always choose to pay its own soldiers and citizens before it pays its foreign bondholders.

Your “guaranteed” return is only guaranteed until it isn’t.

Every major asset class that financial advisors push has a failure rate. They can all go to zero. They can be seized, taxed, or restructured into dust.

Except for one.

For over 5,000 years, from the pharaohs of Egypt to the central banks of today, Gold has never gone bankrupt. It has never defaulted. It’s the only financial asset with a perfect, uninterrupted survival record.

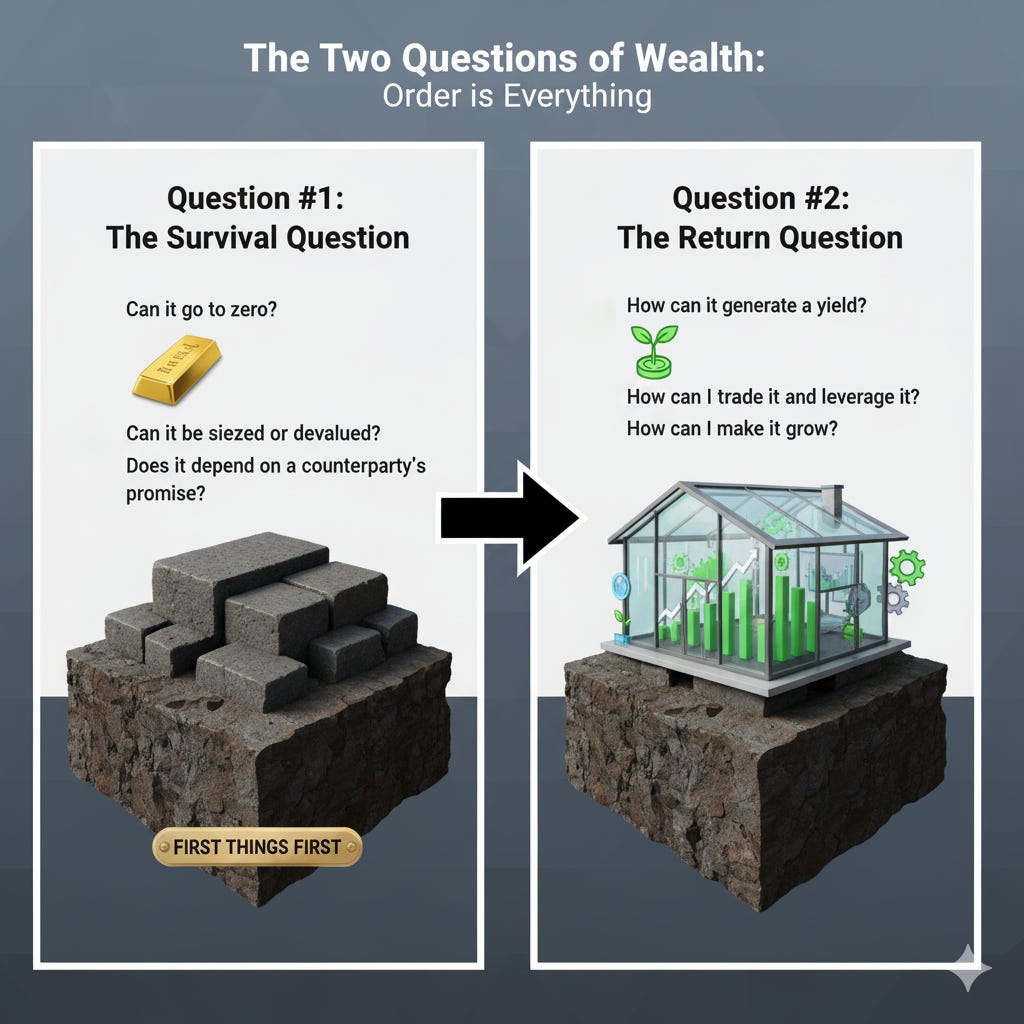

A New Mental Framework: Asking the Right Questions First

The modern financial world has trained you to ask the wrong question. We’re taught to ask, “What’s the return?”

Returns are important. Generating yield is how you build wealth.

The problem isn’t the question itself; it’s the order.

Asking about returns first is like picking out curtains for a house you haven’t built the foundation for yet. A 15% return on an asset that can disappear overnight isn’t a 15% return - it’s a 100% loss with a fancy story.

There are two questions, and their order is everything:

The Survival Question: Can this go to zero? Can it be seized, devalued, or defaulted on? Does it depend on a counterparty promise?

The Return Question: How can I use this asset to generate a yield? How can I trade it, leverage it, and make it grow?

Your base of wealth - the core savings you absolutely cannot afford to lose - must be an answer to Question #1. Physical Gold bullion is the only liquid asset that provides a definitive “No” to the critical parts of that question.

Everything else - stocks, bonds, real estate, even paper Gold - is an answer to Question #2.

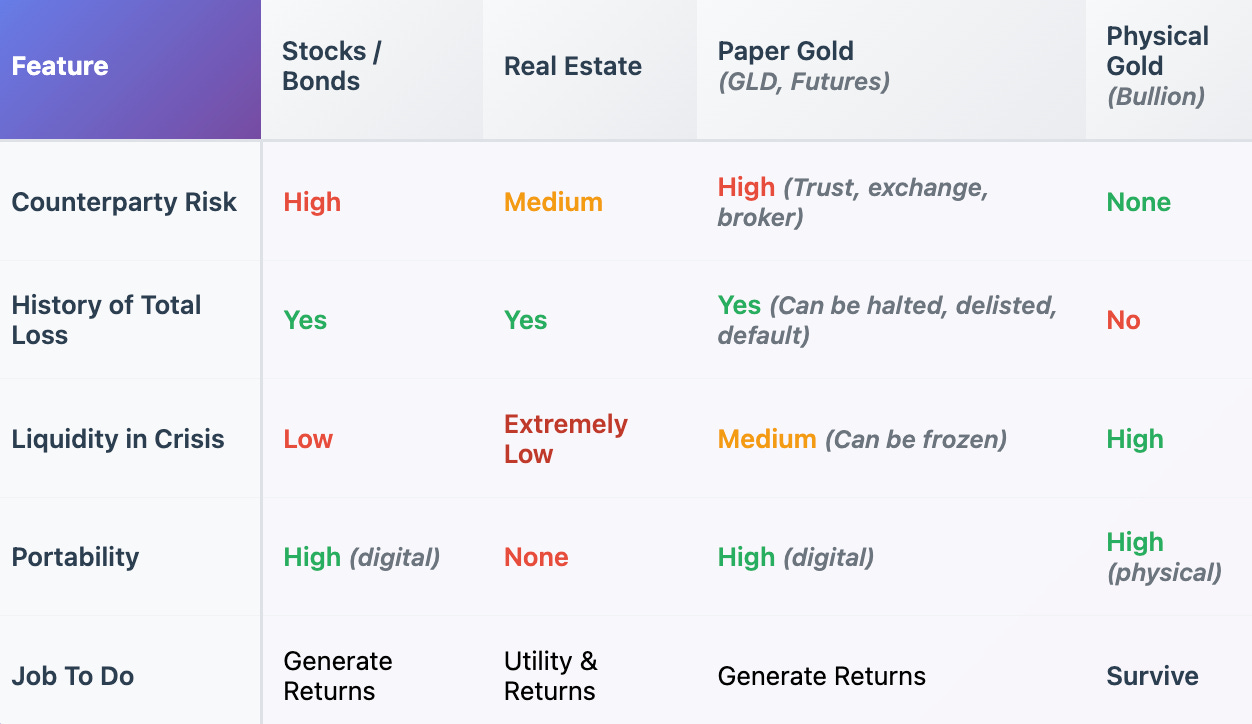

Physical Metal vs. Paper Promises: A Crucial Distinction

This is the next layer of the onion, please stick with me.

The goal is to:

first secure your base wealth in a form that cannot default (physical bullion, stacked month after month),

and then use the IOU system to generate returns.

I trade financial instruments based on Gold all the time. But I never, ever confuse the trade with the metal.

The SPDR Gold Trust ETF (GLD), Gold futures contracts (XAU/USD), mining stocks… these are all IOU Assets. They carry counterparty risk and they’re still several layers removed from touching the actual metal.

These paper instruments are fantastic tools for answering the Return Question. They offer liquidity and convenience.

They do not answer the Survival Question. They exist within the very system of promises you need to insure against.

The bottom like is: The tools you use to get rich are fundamentally different from the one tool you need to stay solvent.

Addressing the Skeptics

“But the U.S. government confiscated gold in 1933!”

Yes, they did. Under Executive Order 6102, FDR forced citizens to turn in their Gold for a fixed price in dollars.

But think about what that actually means. This act isn’t an argument against Gold; it’s the ultimate testament to its power.

The government didn’t confiscate stocks. They didn’t confiscate bonds. They confiscated Gold because it was the only thing that was real money, the only asset that directly competed with their control of the currency.

They had to take it out of the system to devalue the dollar. It proves the whole point.

“But Gold has no yield! It just sits there”

Correct. Physical Gold, that is -the metal in your hand. That is its most important feature.

The demand for a yield is a demand for risk. Your foundation shouldn’t have risk.

The job of your physical Gold is not to “work for you.” Its job is to exist, to hold its value across time, to ensure you can never be wiped out.

It’s the insurance policy on the entire system. And it’s the only one that has never failed to pay out.

2025 and Beyond

The world feels fragile - to say the least. We are facing sovereign debt levels that are mathematically impossible to repay, real estate bubbles across the globe, and stock markets priced for a perfect future that feels increasingly unlikely.

The system of promises is more stretched than it has ever been.

This isn’t about day trading. It’s about building a robust financial life.

You secure the foundation with an asset that can survive anything.

Then, on top of that foundation, you build your house of returns using the powerful, but ultimately riskier, world of paper assets.

When you finally realize that most of what you call “assets” are just digital entries on someone else’s spreadsheet, you start to think differently.

You start to think about what is real, what is permanent, and what you can hold in your hand no matter what happens tomorrow.

Safe trading,

and remember: All that glitters is not Gold,

Joe